Markets

Kirloskar Oil Engines Stock Analysis 2026: India's Engine & Genset Leader on a Roll

Kirloskar Oil Engines (NSE: KIRLOSENG) — KOEL, a flagship of the Kirloskar group has been one of the strongest capital-goods performers of the past year, up over 100%. A near-80-year-old engine and genset maker riding India's infrastructure, power-backup, and defence tailwinds. But after a big run, is there still room to grow, or is the easy money behind us? Here's the quick X-Ray. For data-backed entries, start trading with SEBI registered research analyst backed signals.

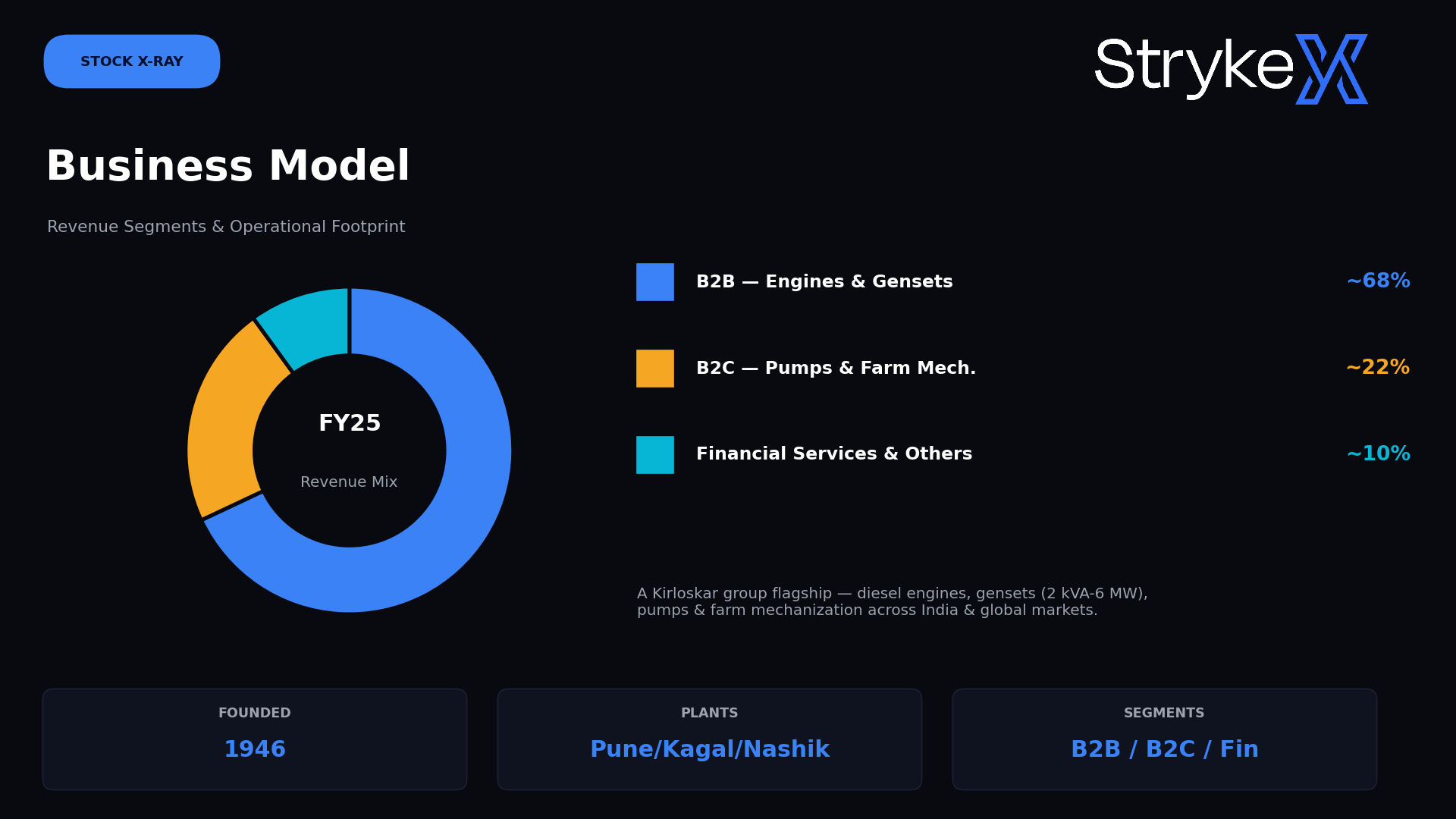

The Company in 30 Seconds

Kirloskar Oil Engines (KOEL) is a flagship Kirloskar group company that manufactures and services diesel engines and diesel generator sets, along with pumps and farm-mechanization products. Founded in 1946 and headquartered in Pune, it makes engines from 2 kVA to 6 MW, serving agriculture, power generation, industrial, telecom, defence, and infrastructure customers in India and globally.

Founded: 1946 (Pune) Promoter Holding: ~41.1% (Kirloskar family) Plants: Pune, Kagal, Nashik

Cross-check the latest numbers on Screener.

Why KOEL Has an Edge

1. Trusted Kirloskar brand — nearly 80 years of engineering heritage and a deep distribution and after-sales network across India. 2. Wide power range — engines and gensets from 2 kVA to 6 MW cover everything from homes and telecom towers to large industrial and institutional clients. 3. Diversified end-markets — agriculture, power backup, infrastructure, hospitality, banks, healthcare, and defence smooth out any single cycle. 4. Conservative balance sheet — low debt and consistent dividends, with profits funding expansion into newer areas.

Want to automate your own trading strategy? Start algo trading with AI-powered robots.

Growth Catalysts to Watch

1. Defence & marine — a Project Sanction Order from the Indian Navy to design a 6 MW medium-speed marine diesel engine opens a high-value, strategic vertical. 2. Power-backup demand — data centres, telecom, real estate, and infrastructure are driving genset demand across the power range. 3. B2B momentum — record quarterly performance with EBITDA-margin expansion in recent quarters. 4. Diversification — moves into clean energy, electric/alternative power, and industrial solutions broaden the long-term runway. 5. Exports & after-sales — a growing international footprint plus a high-margin spares and service business.

Just don't chase a hot run blindly — here are 7 costly trading mistakes to avoid.

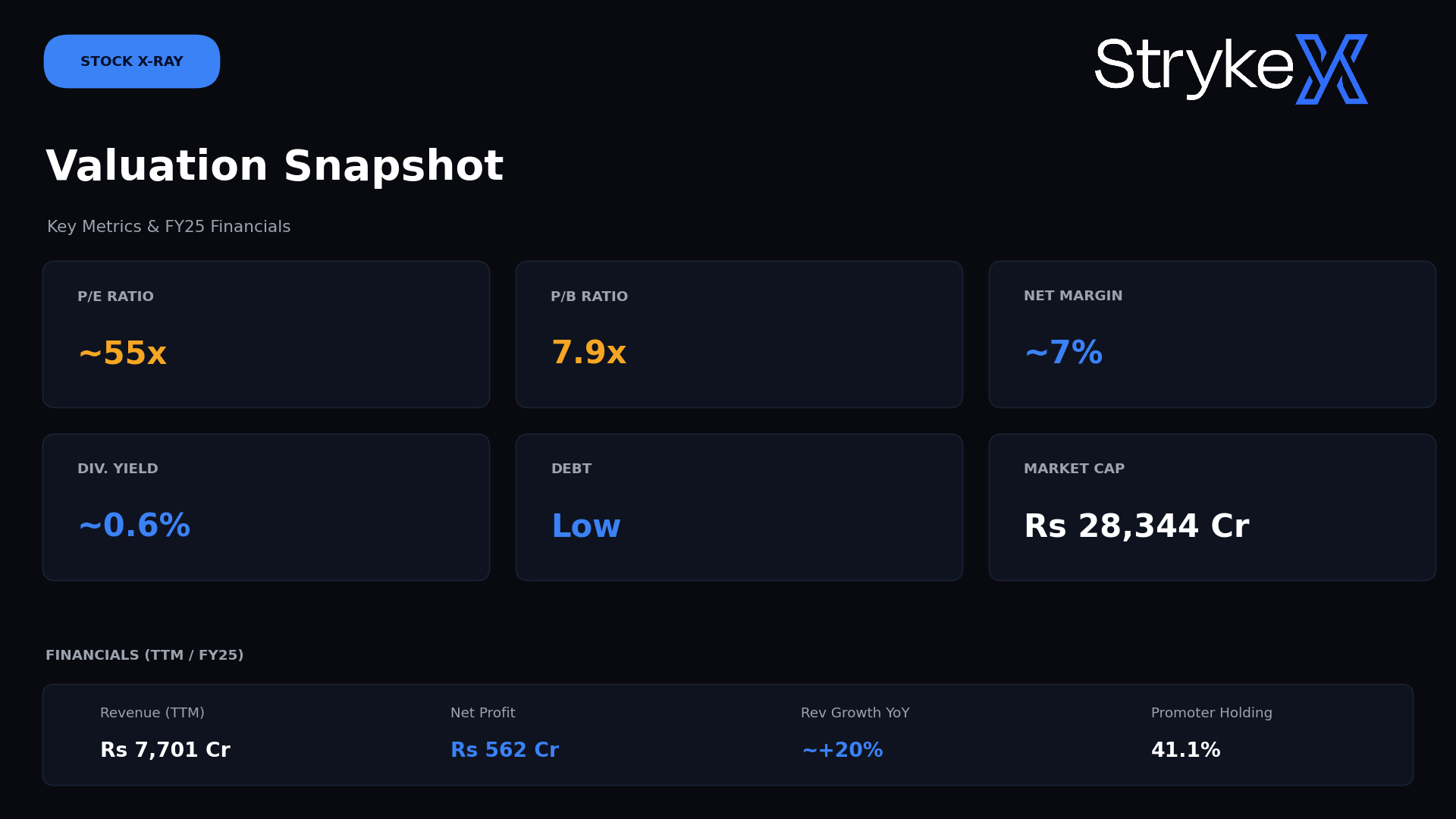

The Numbers

A strong multi-year run — but a stock near its highs after doubling in a year carries elevated valuation risk. New to systematic trading? Start with the complete beginner's guide to algo trading in India.

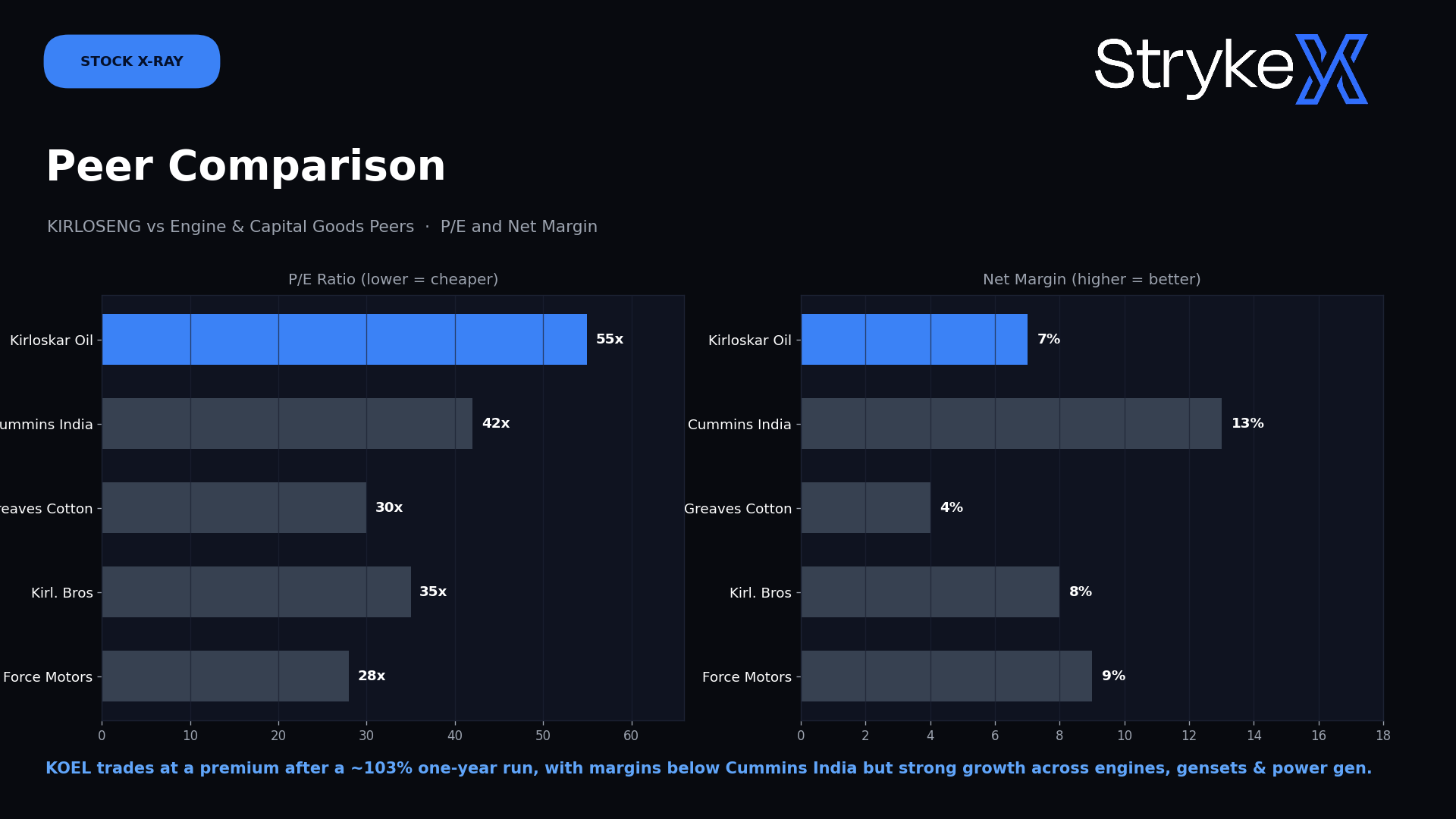

How KOEL Stacks Up

KOEL trades at a premium after its ~103% one-year run. Its net margin sits below market-leader Cummins India but KOEL offers faster recent growth and broad exposure across engines, gensets, and power generation.

Our Take

Bull case: A trusted, diversified Kirloskar flagship with a wide power range, strong distribution, a conservative balance sheet, and fresh catalysts in defence/marine and power backup. Record recent results and margin expansion support the growth story. Bear case: After doubling in a year, it trades at ~55x earnings rich for a capital-goods name with ~7% margins. Earnings are cyclical and sensitive to industrial demand and commodity (steel/input) costs, and recent quarters showed some profit volatility.

Bottom line: A high-quality, diversified engine and power-solutions leader but the valuation has run ahead after a strong rally. Quality business, demanding price. DYOR.

Ready to Act?

1. Create a free trading account 2. Verify fundamentals on Screener 3. Trade with SEBI-registered research analyst signals 4. Automate with AI-powered algo trading

Frequently asked questions

Is Kirloskar Oil Engines a good stock to buy in 2026?

KOEL is a fundamentally strong, diversified engine and genset leader with a trusted Kirloskar brand, low debt, and fresh catalysts in defence and power backup. However, after a ~103% one-year run it trades at a rich ~55x P/E and ~7.9x book, so a lot of optimism is already priced in. It suits long-term investors comfortable with cyclical, capital-goods exposure; valuation-sensitive buyers may prefer better entry points. Always check the latest numbers on Screener and do your own research.

What does Kirloskar Oil Engines do and what is its NSE symbol?

KOEL manufactures and services diesel engines and diesel generator sets (2 kVA to 6 MW), plus pumps and farm-mechanization products, for agriculture, power generation, industrial, telecom, defence, and infrastructure customers. It trades under the symbol KIRLOSENG on NSE (BSE: 533293).

Is Kirloskar Oil Engines part of the Kirloskar group?

Yes. KOEL is one of the flagship companies of the Kirloskar group, with the Kirloskar family holding roughly 41% as promoters. It is distinct from group companies like Kirloskar Brothers, Kirloskar Industries, and Kirloskar Ferrous.

Does Kirloskar Oil Engines pay a dividend?

Yes. KOEL pays regular dividends — it declared ₹2.50 per share in early 2026 translating to a dividend yield of roughly 0.6% at recent prices.

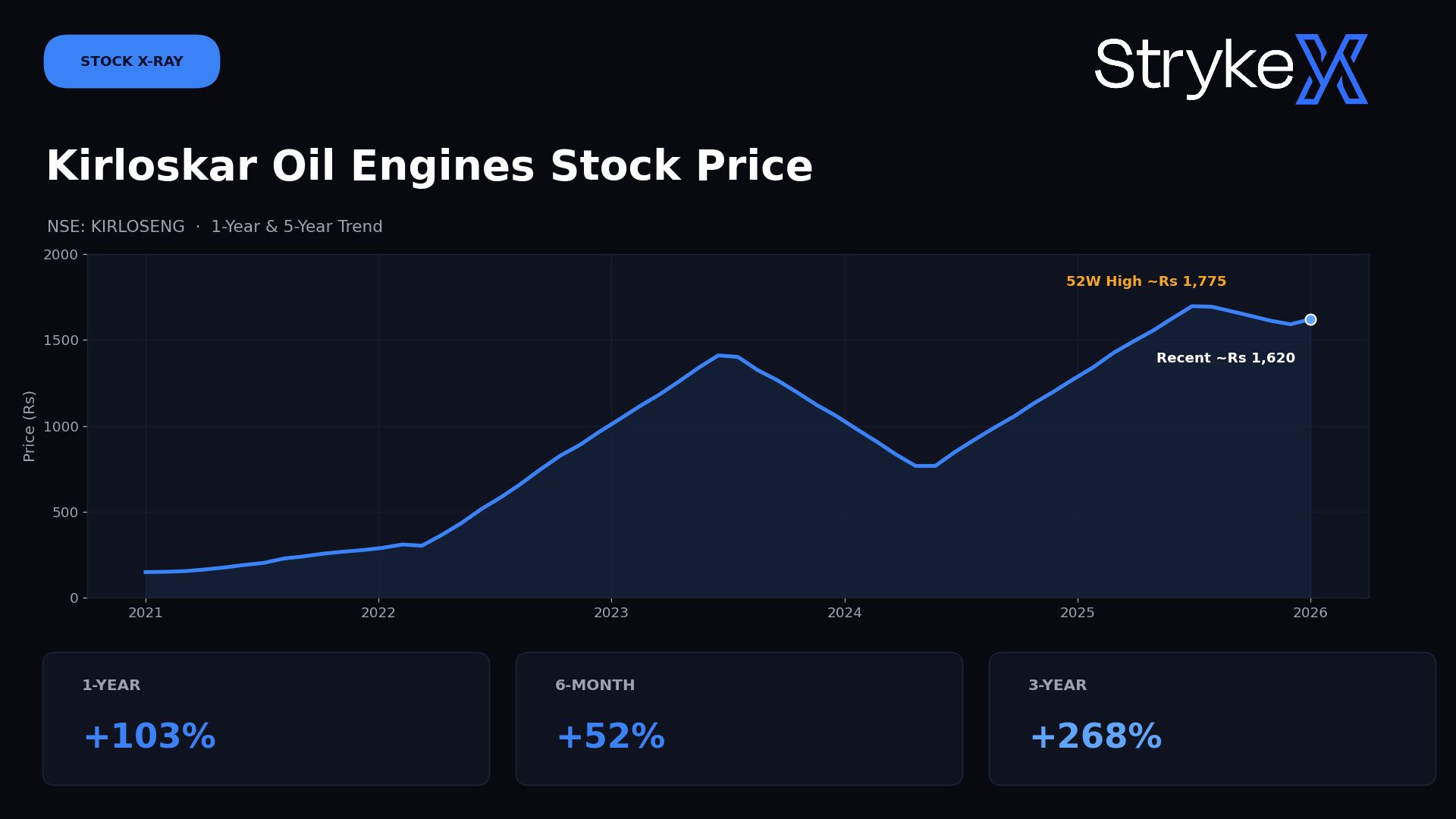

Why has the KIRLOSENG share price risen so much?

The stock is up over 100% in a year, driven by strong B2B growth, margin expansion, record quarterly results and new catalysts like the Indian Navy marine-engine order and rising power-backup demand from data centres and infrastructure.

What are the main risks in Kirloskar Oil Engines stock?

Key risks include its premium valuation after a sharp rally, cyclicality tied to industrial and infrastructure demand, sensitivity to commodity/input costs, competition from domestic and global engine makers and some quarter-to-quarter profit volatility.

How can I start trading or investing in stocks like KIRLOSENG?

You can open a free Demat and trading account to get started, follow SEBI-registered research analyst signals for ideas and automate your strategy with AI-powered algo trading. New to automation? Read the complete beginner's guide to algo trading in India.

StrykeX — Editorial