Trading Strategies

Iron Condor, Straddle, Strangle: Which Works in Which Market?

<p>The first time a trader sees a multi-leg options strategy, it looks like alphabet soup — buy this, sell that, two strikes here, two there. But these structures aren't arbitrary complexity. Each is a tool built for a specific market <em>condition</em>, and the skill isn't memorising the recipes — it's matching the structure to what you think the market is about to do.</p><p><br></p><p>Let's demystify the three you'll meet most, by the situation each is built for. (Education only — these involve real risk, and most retail options traders lose money.)</p>

Iron Condor, Straddle, Strangle: Which Works in Which Market?

<p>The first time a trader sees a multi-leg options strategy, it looks like alphabet soup — buy this, sell that, two strikes here, two there. But these structures aren't arbitrary complexity. Each is a tool built for a specific market <em>condition</em>, and the skill isn't memorising the recipes — it's matching the structure to what you think the market is about to do.</p><p><br></p><p>Let's demystify the three you'll meet most, by the situation each is built for. (Education only — these involve real risk, and most retail options traders lose money.)</p>

First, the mental shift: from direction to movement

<p>Beginners think in direction: <em>up or down?</em> These strategies require a different question: <em>how much will it move, and does direction even matter?</em></p><p><br></p><ul><li>A <strong>straddle</strong> and a <strong>strangle</strong> are bets on <em>big movement</em> — in either direction.</li><li>An <strong>iron condor</strong> is a bet on <em>little movement</em> — the market staying in a range.</li></ul><p><br></p><p>Get that framing and the structures stop being soup and start being sensible.</p>

The straddle: betting on a big move, either way

<p>A long straddle means buying a call and a put at the same strike, usually at-the-money. You're saying: "I think the market is about to move sharply, but I'm not sure which way."</p><p><br></p><ul><li><strong>Profits when:</strong> the underlying moves far enough in either direction to overcome the combined premium you paid.</li><li><strong>Loses when:</strong> the market sits still. Both options decay, and you bleed premium.</li><li><strong>Best for:</strong> events where a big move is likely but direction is genuinely uncertain (e.g. ahead of a major announcement).</li></ul><p><br></p><p>The catch: straddles are expensive (you're buying two options), and the market has to move <em>a lot</em> just to break even. Buy a straddle into an event and watch volatility — and premiums — collapse afterward, and you can lose even if the market moves.</p>

The strangle: a cheaper, wider version of the same bet

<p>A long strangle is like a straddle but using out-of-the-money strikes — a call above and a put below the current price. Cheaper to put on than a straddle, because OTM options cost less.</p><p><br></p><ul><li><strong>Profits when:</strong> the market makes a <em>large</em> move in either direction.</li><li><strong>Loses when:</strong> the market stays within the gap between your two strikes.</li><li><strong>Best for:</strong> expecting a very big move, wanting lower upfront cost than a straddle</li></ul><p><br></p><p>The trade-off versus a straddle: you pay less, but the market has to move even <em>further</em> before you profit, because your strikes are further out.</p>

The iron condor: getting paid for nothing happening

<p>The iron condor flips the logic. Instead of betting on a big move, you bet the market <em>stays in a range</em>. It's built from selling an OTM call spread and an OTM put spread — collecting premium from both, with defined risk on each side.</p><p><br></p><ul><li><strong>Profits when:</strong> the underlying stays between your inner strikes through expiry, letting the options you sold decay.</li><li><strong>Loses when:</strong> the market breaks sharply out of your range.</li><li><strong>Best for:</strong> calm, range-bound markets where you expect low movement, and you want time decay working <em>for</em> you.</li></ul><p><br></p><p>The appeal is the "income from a quiet market" framing. The danger is that range-bound markets don't stay range-bound forever, and a sharp breakout can hand you a loss that wipes out many quiet months of small gains. Defined risk means the loss is capped — but capped can still be large relative to the premium collected.</p>

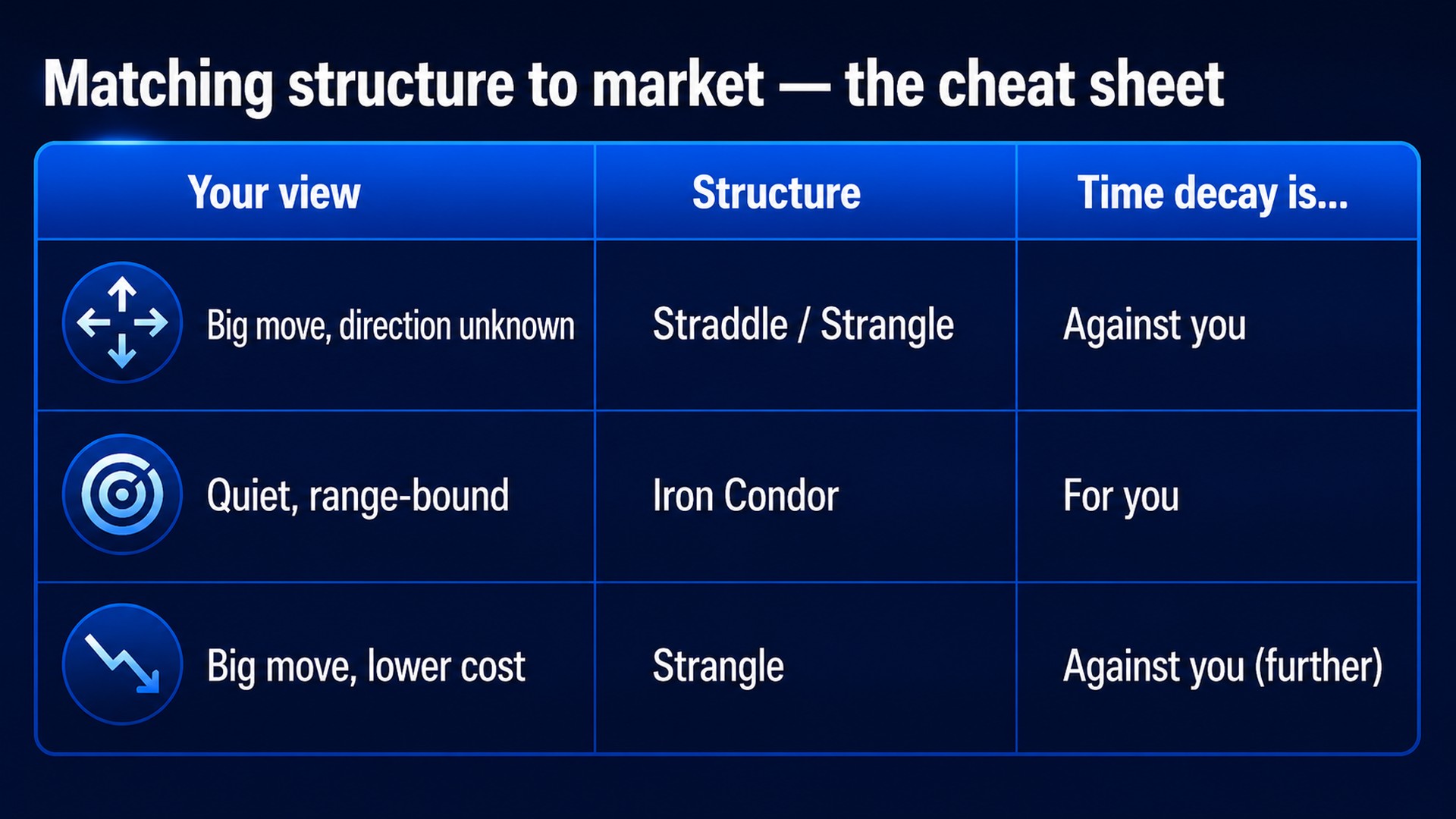

Matching structure to market — the cheat sheet

<p>The single most useful insight: <strong>straddles and strangles want movement; condors want stillness.</strong> If you put on a condor and the market explodes, or buy a straddle and the market naps, you've matched the wrong tool to the conditions — which is the most common way these strategies lose.</p>

A reality check on execution

<p>These are <em>multi-leg</em> strategies. Two, three, four orders per position, plus adjustments. Every leg carries brokerage and slippage, and the STT increase from April 2026 adds to the drag. A condor's modest premium can be meaningfully eroded by sloppy execution across four legs — which is one reason traders automate the entry and adjustment of these structures rather than clicking each leg manually. More on that in how algos execute options adjustments.</p><p><br></p><p>Whichever you trade, understand the [Greeks] first — these structures are most easily understood through how their combined delta, theta, and vega behave. And size every one of them with real risk management.</p><p><br></p><p>For the full options picture, see the options strategies guide for India.</p>

StrykeX — By Stockwiz Technologies