Markets

IMFA Stock Analysis 2026: India's Ferro Chrome Leader Powering the Stainless Steel Story

<p>Indian Metals & Ferro Alloys<span style="color: rgb(17, 17, 17);"> (NSE: IMFA) </span> India's largest fully integrated ferro chrome producer has quietly delivered one of the strongest multi-year runs in the metals space, up well over 100% in the past year. A backward-integrated player that owns its mines and power, selling into the global stainless-steel chain. But after a sharp rally and some margin pressure, is there still value here? Here's the quick X-Ray. For data-backed entries<span style="color: rgb(17, 17, 17);">, start trading with SEBI registered research analyst backed signals.</span></p>

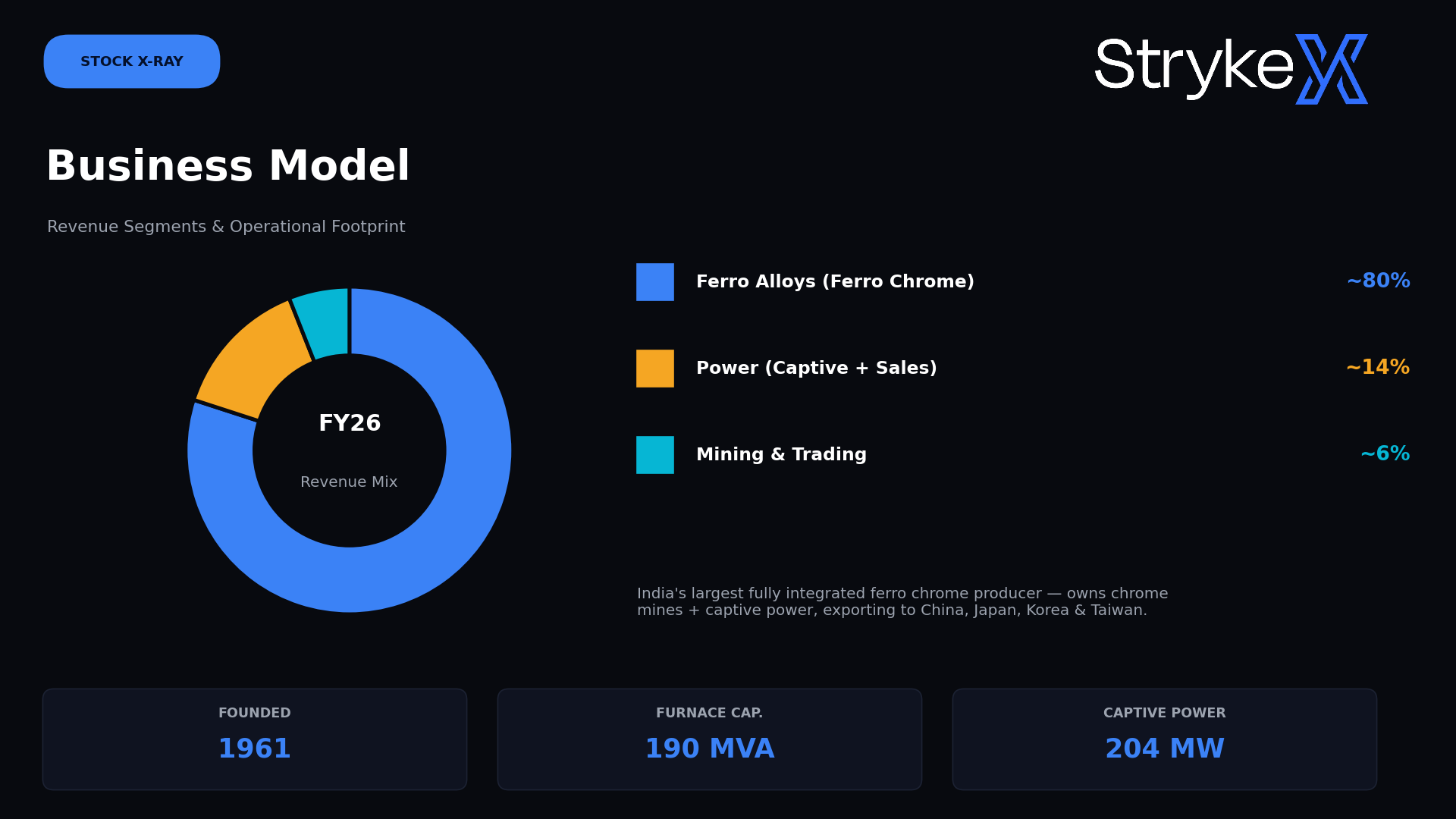

The Company in 30 Seconds

<p>Indian Metals & Ferro Alloys (IMFA), set up in 1961 and headquartered in Bhubaneswar, is <strong>India's largest fully integrated producer of ferro chrome</strong> — a key input for stainless steel. Its operations span the entire chain: chrome ore mining, beneficiation, smelting, refining, and fabrication, backed by captive power. It accounts for roughly 20% of India's ferro chrome output and a quarter of exports.</p><ul><li><strong>Founded:</strong> 1961 (Odisha)</li><li><strong>Promoter Holding:</strong> ~58.7%</li><li><strong>Furnace / Power:</strong> 190 MVA furnaces + ~204 MW captive power</li></ul><p>Cross-check the latest numbers on<span style="color: rgb(17, 17, 17);"> Screener</span>.</p>

Why IMFA Has an Edge

<p>Full backward integration — owning chrome mines and captive power gives consistent quality and strong cost control versus non-integrated rivals.</p><p>Market leadership — India's largest integrated ferro chrome maker, with ~20% of output and ~25% of exports.</p><p>Strong balance sheet — low debt, healthy cash, and a consistent dividend track record.</p><p>Captive power moat — ~204 MW of captive generation (including solar) cushions energy costs, a major input for smelting.</p><p>Want to automate your own trading strategy? Start algo trading with AI-powered robots.</p>

Growth Catalysts to Watch

<p>1. Capacity expansion — ferro chrome capacity ramping toward ~5 lakh TPA, targeting output of around 400,000 tons in FY27.</p><p>2. Renewable power — a 26% stake in EG Urja Strot (₹110 Cr) secures 65 MW of hybrid green power under a captive model, cutting costs and carbon.</p><p>3. Ethanol foray — diversification into ethanol production adds a new, policy-supported revenue stream.</p><p>4. Stainless-steel demand — structural growth in global and Indian stainless-steel consumption underpins ferro chrome demand.</p><p>5. Cost efficiency — management guides for EBITDA cost-per-ton reductions as new units (KNR 1 & 2) fully ramp by FY27.</p><p>Just don't chase a hot run blindly — here are 7 costly trading mistakes to avoid.</p>

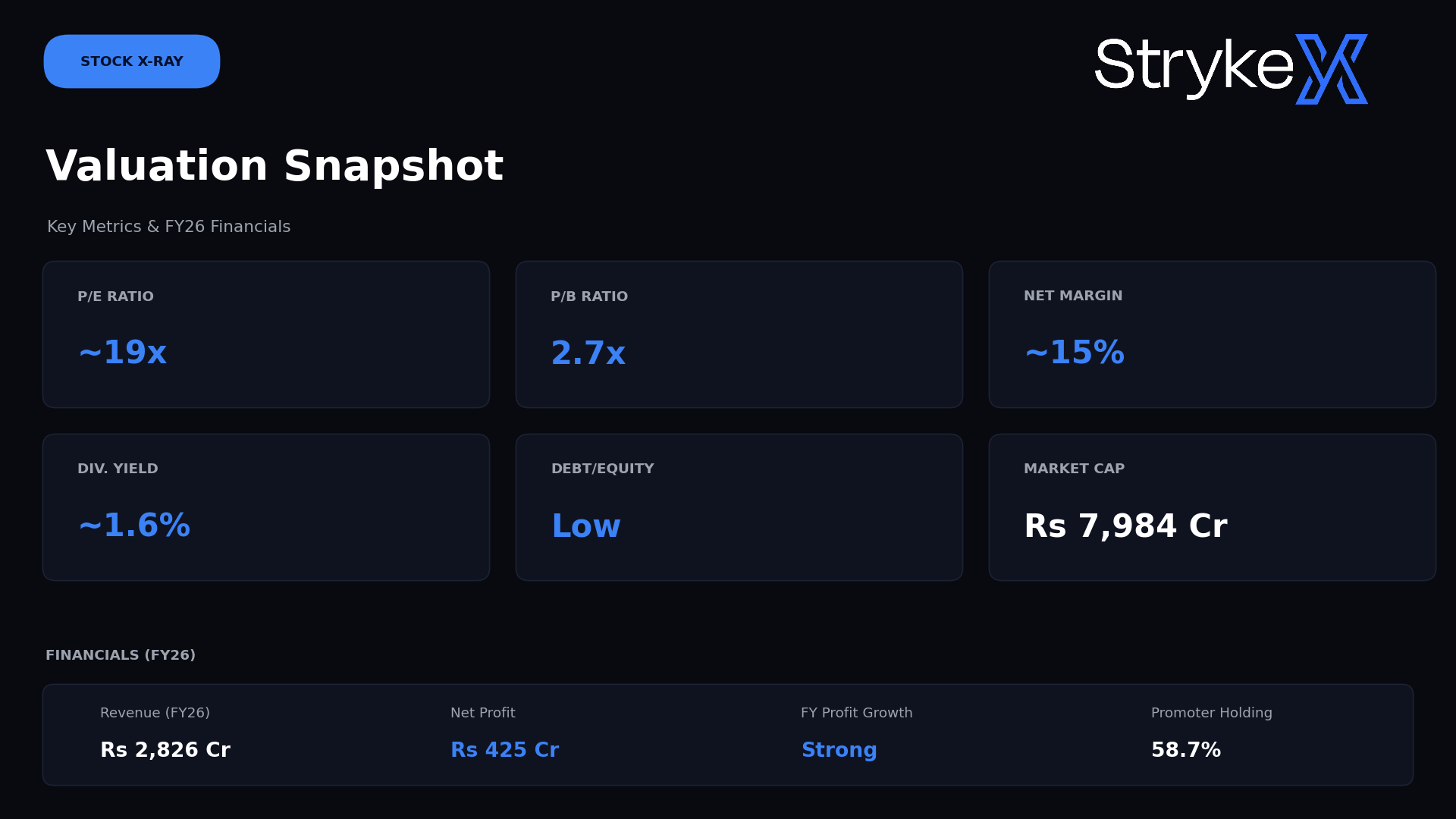

The Numbers

A strong multi-year run but a cyclical commodity stock near its highs carries elevated risk if ferro chrome prices soften. New to systematic trading? Start with the complete beginner's guide to algo trading in India.

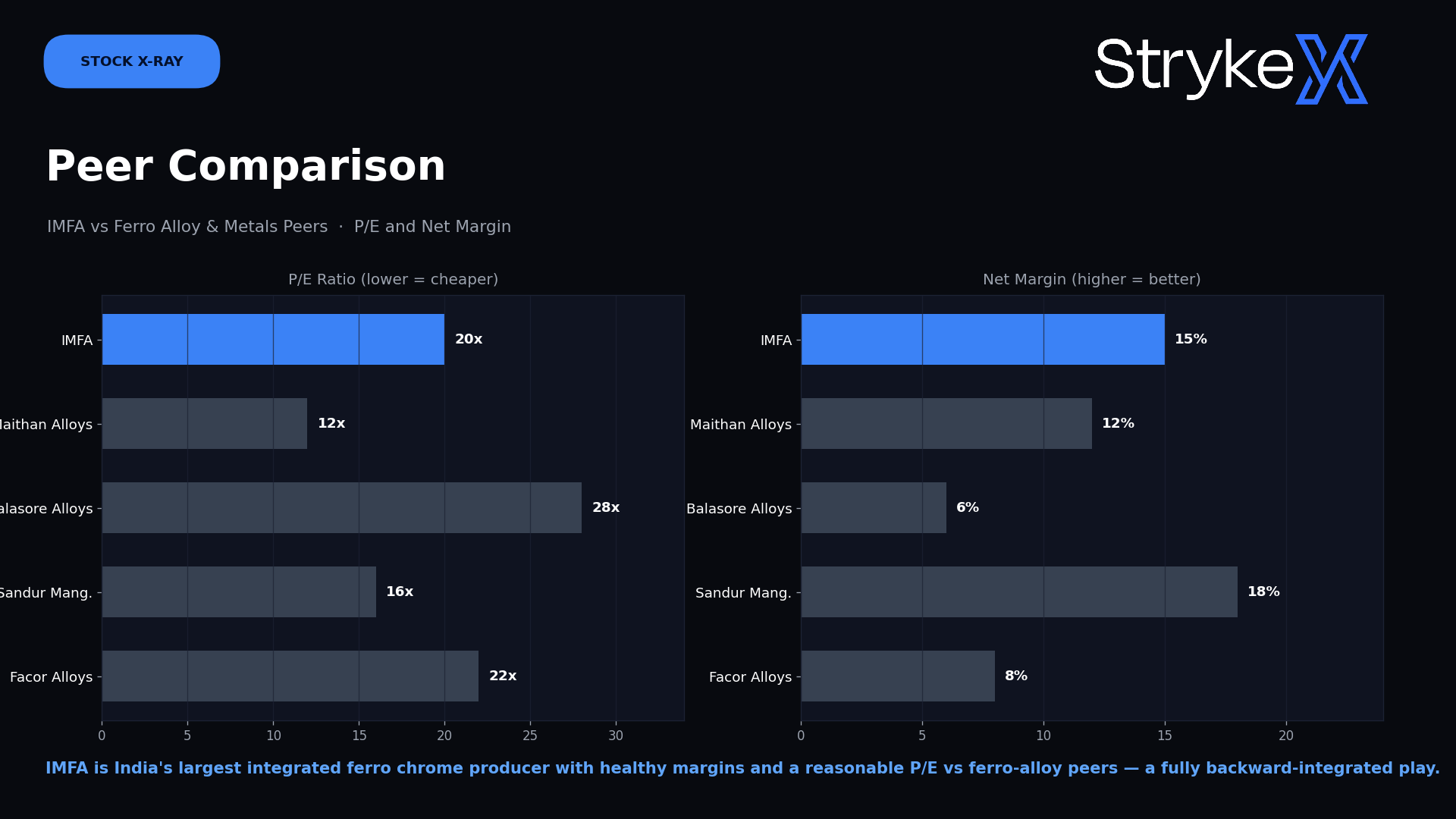

How IMFA Stacks Up

IMFA stands out as India's only large fully integrated ferro chrome player, with healthy margins and a reasonable P/E versus ferro-alloy peers like Maithan Alloys. Its mine-to-power integration is hard to replicate.

Our Take

<p>Bull case: India's leading integrated ferro chrome producer with mine and power ownership, strong margins, low debt, consistent dividends and growth from capacity expansion plus green-power and ethanol diversification. A reasonably valued metals compounder.</p><p>Bear case: Ferro chrome is a cyclical commodity earnings swing with global chrome prices, stainless-steel demand (especially China), and input/power costs. Q4 FY26 already showed sequential margin compression, and the stock has run hard.</p><p>Bottom line: A high-quality, integrated commodity leader at a reasonable valuation but remember it's cyclical, so entry price and the chrome cycle matter. DYOR.</p>

Ready to Act?

<p>1. Create a free trading account</p><p>2. Verify fundamentals on Screener</p><p>3. Trade with SEBI-registered research analyst signals</p><p>4. Automate with AI-powered algo trading</p>

Frequently asked questions

Is IMFA a good stock to buy in 2026?

IMFA is a fundamentally strong, fully integrated ferro chrome leader with low debt, healthy ~15% margins, consistent dividends, and a reasonable ~19x P/E. However, it's a cyclical commodity stock that has rallied ~139% in a year, so earnings and the share price can swing with global chrome prices and stainless-steel demand. It suits investors comfortable with commodity cyclicality; mind the entry point and the cycle. Always check the latest numbers on Screener and do your own research.

What does IMFA do and what is its NSE symbol?

IMFA (Indian Metals & Ferro Alloys) is India's largest fully integrated producer of ferro chrome, a key input for stainless steel. It owns chrome mines and captive power, and exports to China, Japan, South Korea, and Taiwan. It trades under the symbol IMFA on NSE (BSE: 533047).

Is IMFA profitable and does it pay a dividend?

Yes. IMFA reported FY26 revenue of about ₹2,826 crore and net profit of around ₹425 crore. It pays regular dividends and recommended a ₹7.50 final dividend for FY26, giving a yield of roughly 1.6% at recent prices.

Why has the IMFA share price risen so much?

The stock is up over 100% in a year, driven by strong profit growth, improved ferro chrome realisations, margin expansion in earlier quarters, capacity expansion plans, and diversification into renewable power and ethanol.

What are the main risks in IMFA stock?

Key risks include commodity cyclicality (ferro chrome and chrome ore prices), dependence on stainless-steel demand especially from China, power and input cost volatility, export-market and currency risk, and recent quarterly margin compression.

How can I start trading or investing in stocks like IMFA?

You can open a free Demat and trading account to get started, follow SEBI-registered research analyst signals for ideas and automate your strategy with AI-powered algo trading. New to automation? Read the complete beginner's guide to algo trading in India.

StrykeX — Editorial