Market Updates

GMDC Stock Analysis 2026: Is This PSU Mining Gem Still a Buy?

Gujarat Mineral Development Corporation (NSE: GMDCLTD) is up +137% in a year — zero debt, government-backed, and sitting on a rare-earth treasure chest. But after that run, is there still upside left? Here's the quick X-Ray. For data-backed entries, start trading with SEBI registered research analyst backed signals.

GMDC Stock Analysis 2026: Is This PSU Mining Gem Still a Buy?

StockWiz Research Desk | 2026 | 4 min read

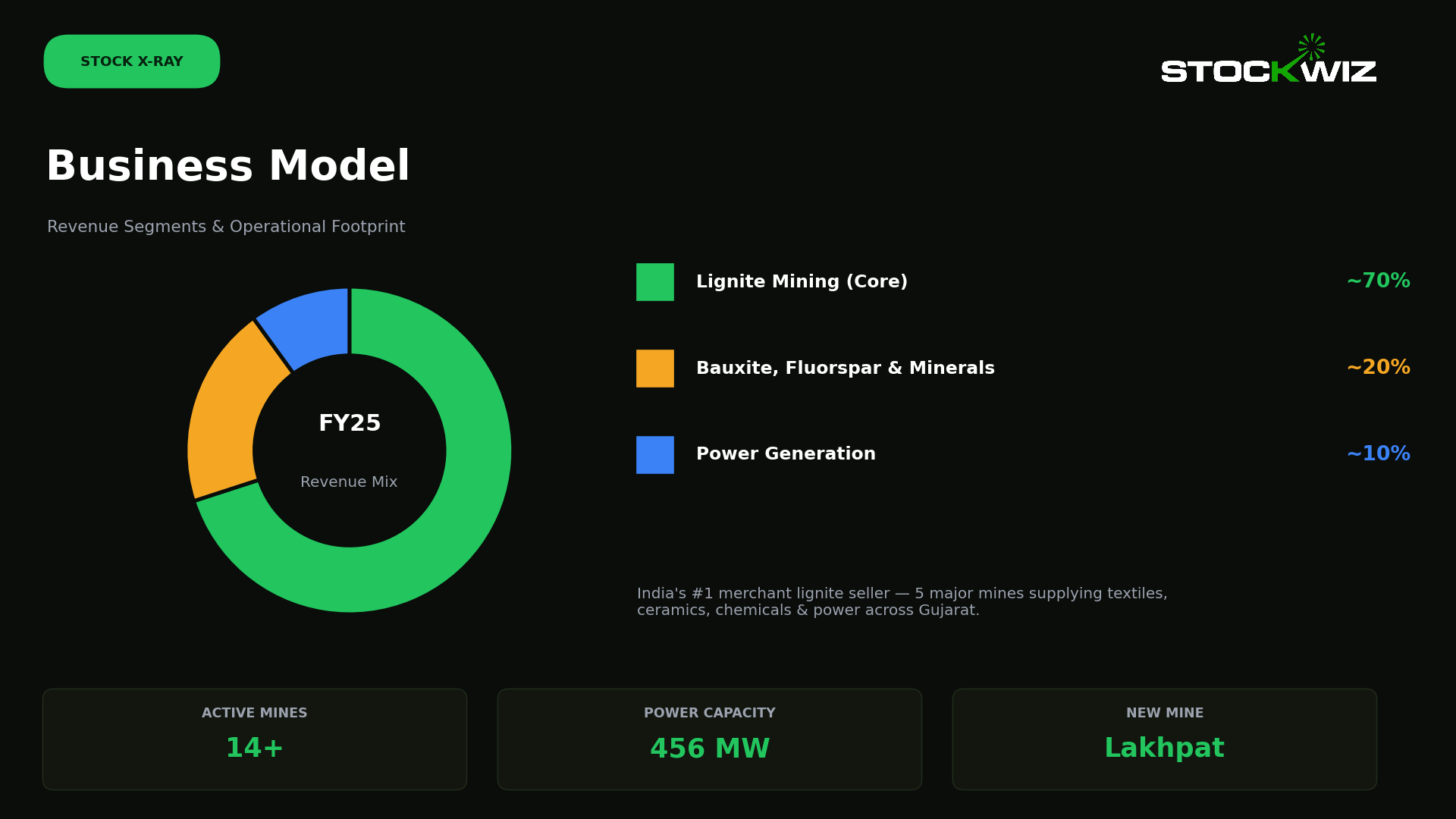

The Company in 30 Seconds GMDC is India's second-largest lignite producer, a Government of Gujarat PSU (74% stake) founded in 1963 — now expanding aggressively into Rare Earth Elements, Odisha coal, and renewables. • Promoter Stake: 74% (Govt of Gujarat) • Balance Sheet: Zero debt • Dividend Yield: ~3% Cross-check the latest numbers on Screener. Revenue mix: Lignite mining ~70%, minerals (bauxite/fluorspar) ~20%, power ~10%. 14+ active mines, 456 MW capacity, new Lakhpat mine coming online.

Why GMDC Has an Edge

• Govt backing (74%) — preferential mining leases, near-zero competition for core mines. • Lignite near-monopoly — India's largest merchant lignite seller, 60+ years, irreplaceable supply chain. • Zero debt + ~3% dividend — strong cash through commodity cycles. • Rare Earth Elements — Ambadungar deposit + NMDC MoU + the govt's ₹7,280 Cr rare earth scheme = a potential re-rating trigger. Want to automate the hunt for stocks like this? Start algo trading with AI-powered robots. Growth Catalysts to Watch 1. Rare Earth (Ambadungar) — biggest re-rating trigger via the ₹7,280 Cr scheme. 2. New mines — Lakhpat approved (3 MTPA lignite + 29.8 MTPA limestone), three more slated. 3. Project Disha — 250 MW ATPS plant revamped, restoring a long-time profit drag. 4. Odisha coal + NTPC MoU — Kudanali Lubri block (468 MT) opens a new revenue stream. 5. 4X growth vision — wind/solar expansion + 68/100 ESG rating. Just don't chase momentum blindly — here are 7 costly trading mistakes to avoid.

The Numbers

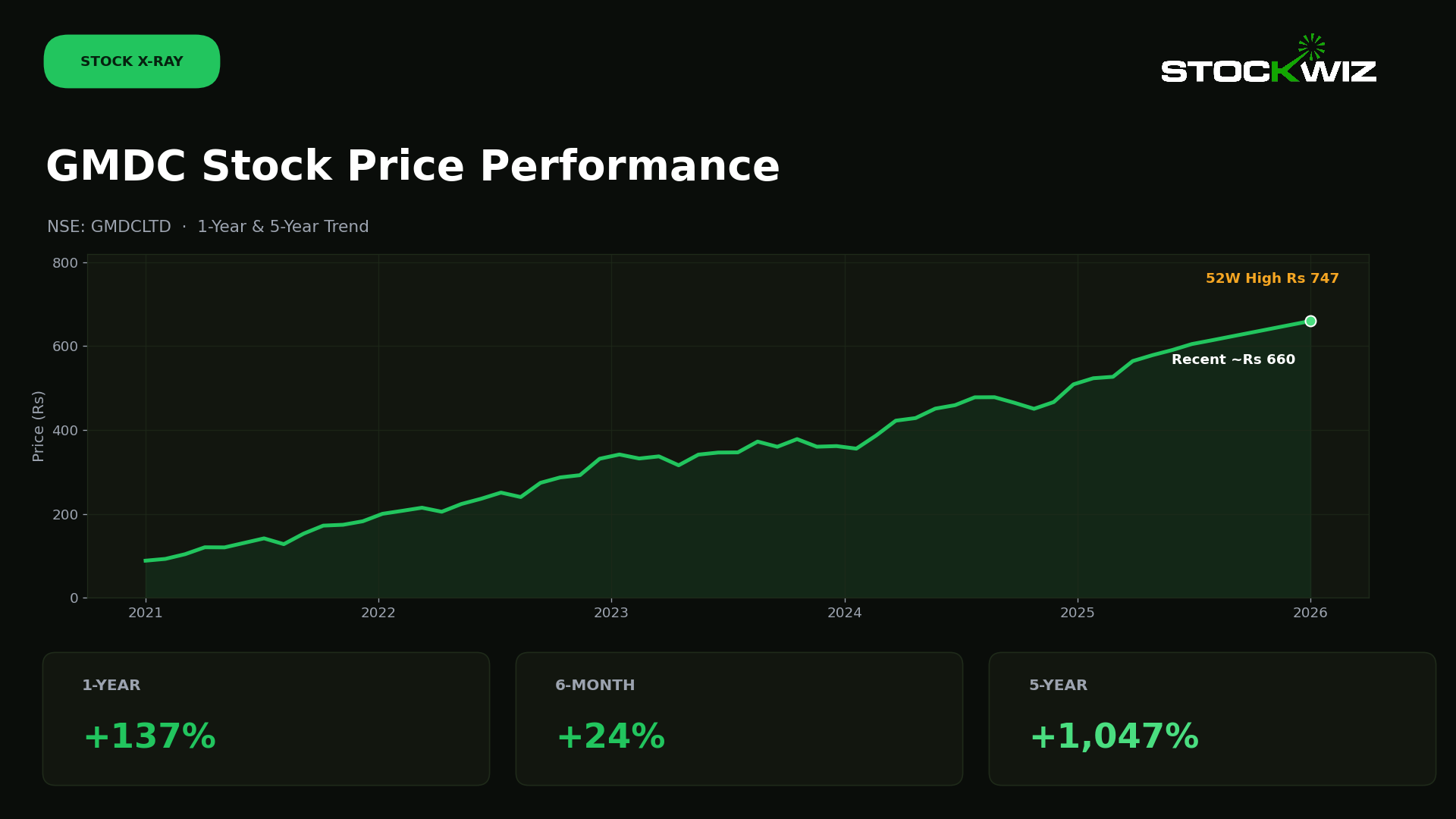

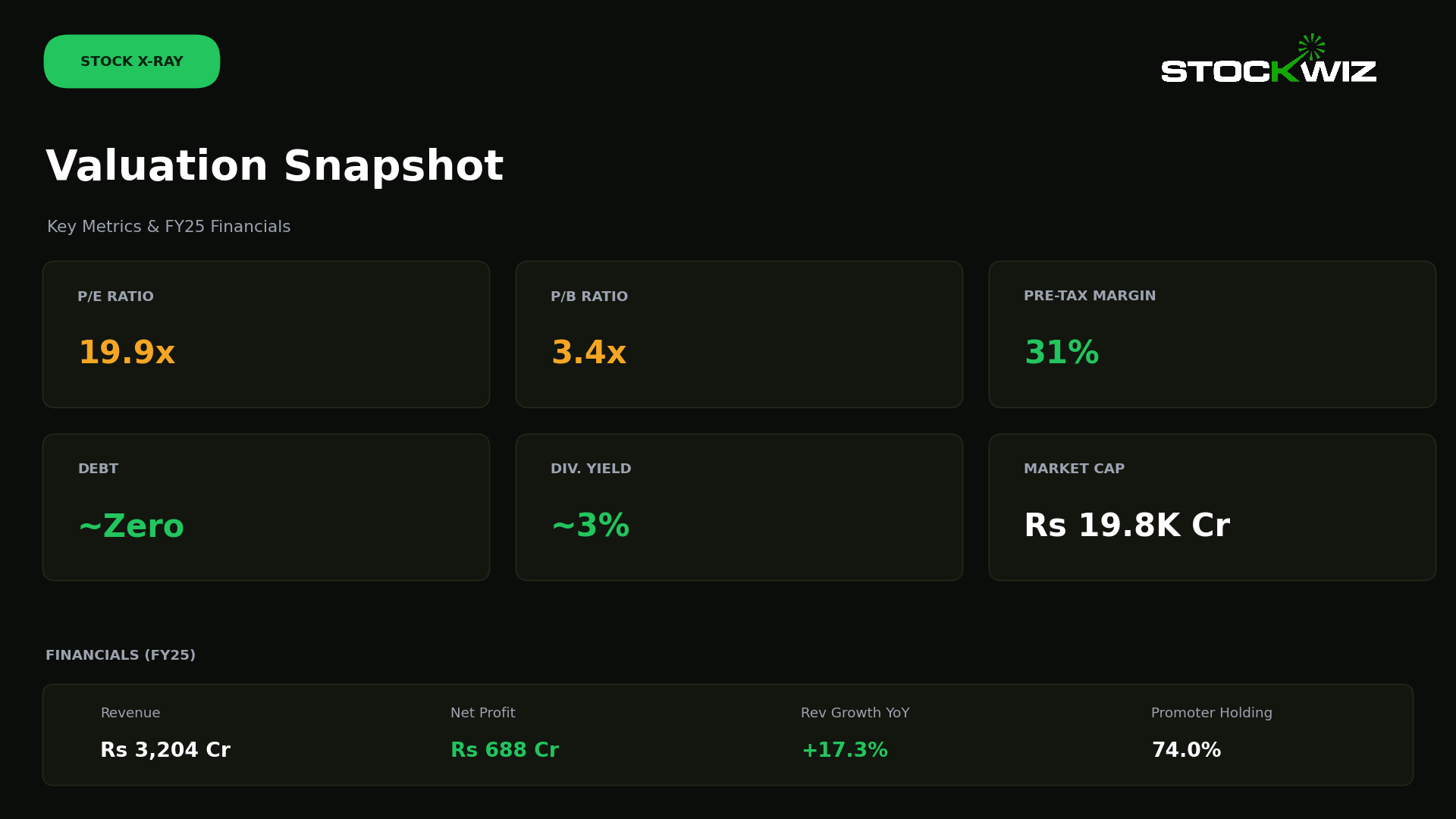

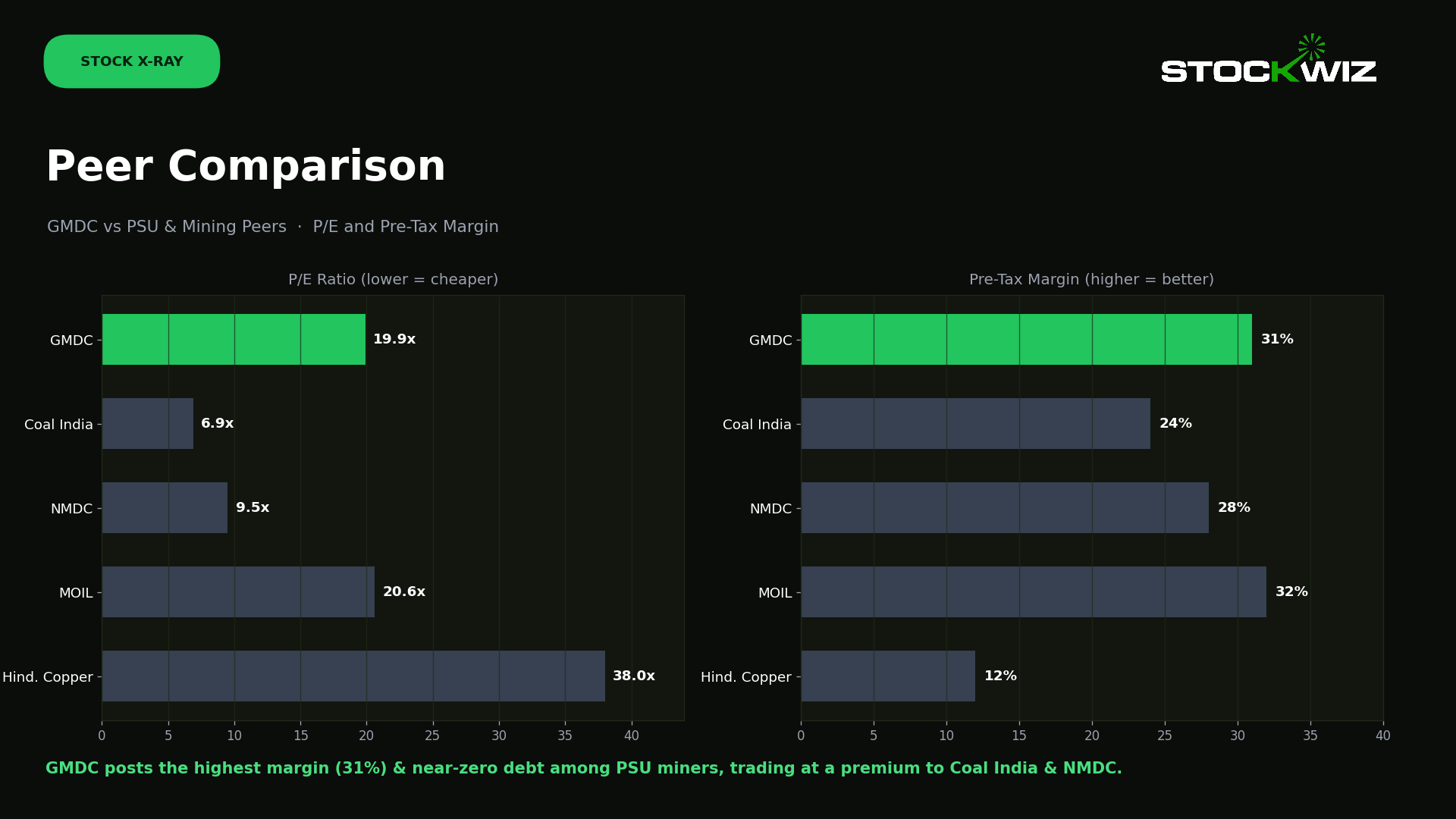

Returns: +24% (6M), +137% (1Y), +1,047% (5Y). 52-week range: ₹280–₹747. A genuine multi-bagger — but trading near its 52-week high after +137% means new buyers aren't getting a discount. New to systematic trading? Start with the complete beginner's guide to algo trading in India. P/E ~19.9x, P/B ~3.4x, pre-tax margin 31%, market cap ~₹19.8K Cr. FY25: revenue ₹3,204 Cr, net profit ₹688 Cr (+17.3% YoY). How GMDC Stacks Up Compare on Screener: GMDC · Coal India · NMDC · MOIL · Hindustan Copper GMDC has the highest pre-tax margin (31%) and near-zero debt among PSU miners. It trades at a premium to Coal India (6.9x P/E) and NMDC (9.5x) but its REE optionality and 4X vision arguably justify it.

Our Take

Bull case: Zero debt, 31% margins, dividend-paying, with a rare-earth treasure chest and a credible 4X growth roadmap. Bear case: After +137%, it trades at a premium to peers. Near-term upside is limited unless REE catalysts land, and lignite faces long-term energy-transition headwinds. Bottom line: A quality PSU compounder for the long term — but exercise valuation caution near-term. DYOR. Ready to Act? 1. Create a free trading account 2. Verify fundamentals on Screener 3. Trade with SEBI-registered research analyst signals 4. Automate with AI-powered algo trading

P/E ~19.9x, P/B ~3.4x, pre-tax margin 31%, market cap ~₹19.8K Cr. FY25: revenue ₹3,204 Cr, net profit ₹688 Cr (+17.3% YoY).

How GMDC Stacks Up

Compare on Screener: GMDC · Coal India · NMDC · MOIL · Hindustan Copper

Frequently asked questions

Is GMDC a good stock to buy in 2026?

GMDC is a fundamentally strong PSU — zero debt, 31% pre-tax margins, ~3% dividend yield, and Government of Gujarat backing (74%). However, after a +137% one-year rally it trades at ~19.9x P/E, a premium to peers like Coal India and NMDC. It suits long-term investors who believe in the rare-earth story; near-term buyers should be mindful of valuation. Always verify the latest numbers on Screener and do your own research.

What does GMDC (Gujarat Mineral Development Corporation) do?

GMDC is India's second-largest lignite producer and the largest merchant seller of lignite. Roughly 70% of revenue comes from lignite mining, ~20% from bauxite, fluorspar and other minerals, and ~10% from power generation. It is also expanding into Rare Earth Elements, Odisha coal mining, and renewable energy.

Is GMDC debt-free?

Yes. GMDC has a near-zero-debt balance sheet (D/E ~0.02x), which gives it strong financial flexibility and the ability to fund expansion and pay consistent dividends through commodity cycles.

Why has the GMDC share price risen so much?

The stock is up +137% in one year and +1,047% over five years, driven by its rare-earth optionality (the Ambadungar deposit + NMDC MoU + the government's ₹7,280 Cr rare earth magnet scheme), new mine approvals like Lakhpat, the Project Disha power-plant turnaround, and its entry into Odisha coal with an NTPC supply agreement.

What are the main risks in GMDC stock?

Key risks include a premium valuation versus PSU mining peers, long-term energy-transition headwinds for lignite (demand may soften post-2030), the ongoing ATPS power-plant turnaround, and an uncertain timeline for the rare-earth catalysts to actually translate into earnings.

What is GMDC's dividend yield and promoter holding?

GMDC offers a dividend yield of approximately 3%, and the Government of Gujarat holds about 74% as promoter a sign of strong government backing.

How can I start trading or investing in stocks like GMDC?

You can open a free Demat and trading account to get started, follow SEBI-registered research analyst signals for ideas, and even automate your strategy with AI-powered algo trading. New to automation? Read the complete beginner's guide to algo trading in India.

StrykeX — Editorial