Market Updates

5 Indian Stocks That Could Transform Your Portfolio in 2026

5 high-conviction picks for 2026: MTAR Technologies (Bloom 7x + Nuclear), Lloyds Metals (55 MTPA iron ore), Atlanta Electricals (3.8x transformer capacity), GE Power India (19x P/E + JSW demerger), Indo Tech Transformers (30% ROE, cheapest in segment). Backed by ₹11.1L Cr infra budget & India’s transformer supercycle.

5 Indian Stocks That Could Transform Your Portfolio in 2026

5 high-conviction picks for 2026: MTAR Technologies (Bloom 7x + Nuclear), Lloyds Metals (55 MTPA iron ore), Atlanta Electricals (3.8x transformer capacity), GE Power India (19x P/E + JSW demerger), Indo Tech Transformers (30% ROE, cheapest in segment). Backed by ₹11.1L Cr infra budget & India’s transformer supercycle.

🏦 Ready to invest in these high-conviction stocks? Open Your Free Demat Account with Dhan — Zero-Cost Setup, Invest in MTAR, Lloyds & More → 100% free. API-ready broker integrates with StyrkeX algo platform.

MTAR Technologies (MTARTECH) — Precision Engineering Monopoly

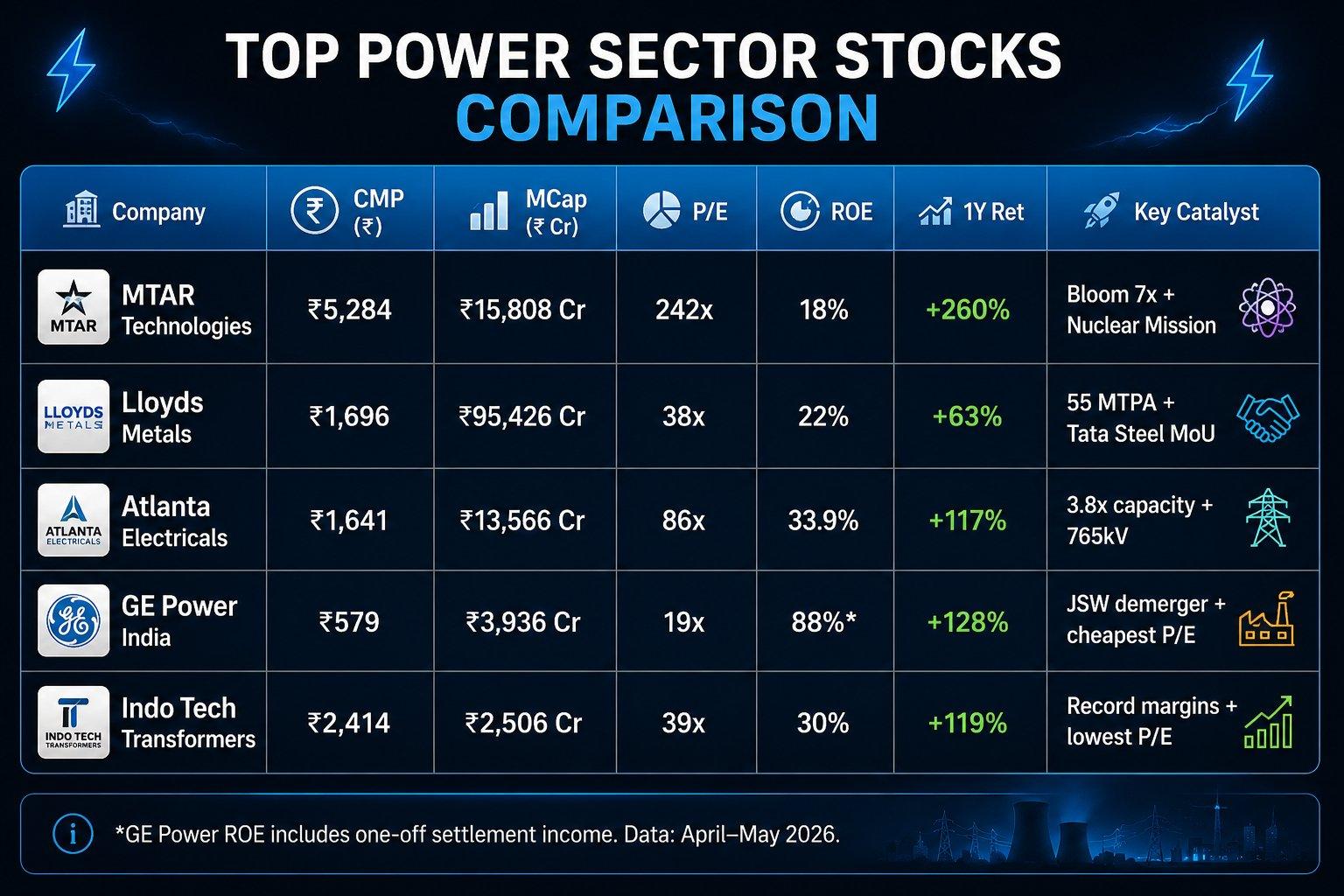

MTARTECH CMP ₹5,284 | MCap ₹15,808 Cr | Aerospace & Defence

• Core business: Ultra-precision components (±2 micron) for nuclear, rockets, defence & fuel cells. Sole supplier once qualified — enormous switching costs. • Bloom Energy (USA): Exclusive Indian supplier. 7x capacity expansion by FY28. Revenue: ₹250–300 Cr → ₹1,500–2,000 Cr (5–7x jump) • Nuclear + ISRO: NPCIL supplier 55 years | Kaiga 5&6: ₹504 Cr + ₹310 Cr | Liquid propulsion & cryogenic pumps on every ISRO mission • Q3 FY26: Revenue ₹278 Cr (+59%) | EBITDA ₹64 Cr (record) | PAT +117% at ₹34.7 Cr | Order Book ₹2,800 Cr (3.5x run-rate)

⚠️ Risk: 242x P/E. Bloom = ~45% revenue. Q2 FY26: PAT -77% YoY, stock fell ₹3,500+ → ₹1,358.

📞 MTAR at 242x P/E — how do you size the position? Book a Free 1-on-1 Stock Analysis Call — Personalised Entry Strategy for MTAR & High-Conviction Picks →

Position-sizing strategy tailored to your capital, risk, and horizon.

Lloyds Metals & Energy (LLOYDSME) — India’s Iron Ore Mega Story

LLOYDSME CMP ₹1,696 | MCap ₹95,426 Cr | Mining / Iron Ore

• Surjagarh Mine: Fe 63–65% high-grade, Gadchiroli. EC to expand 10 MTPA → 55 MTPA (5.5x) — one of Asia’s largest single mines • Integrated strategy: Tata Steel MoU | 4 MTPA pellet plant (100% utilisation) | 950 km slurry pipeline cuts logistics 40–50% • FY25 financials: ₹12,286 Cr revenue | ₹2,500 Cr PAT | Net debt-free | Stock +63% | Projection: ₹27,000 Cr cumulative FY26–28

⚠️ Risk: Single-mine concentration (Gadchiroli security). ₹33,000 Cr capex over 5 years. 38x P/E.

Atlanta Electricals (ATLANTAELE) — Transformer Supercycle’s Fastest Mover

ATLANTAELE | CMP ₹1,641 | MCap ₹13,566 Cr Power / Transformers

• Capacity: 16,740 MVA → 63,060 MVA (3.8x) in 12 months via Vadod plant + BTW-Atlanta acquisition. FY26 volume +105% YoY • 765 kV / 500 MVA: Only 4–5 Indian companies — unlocks HVDC supergrid contracts worth thousands of crores • Metrics: ROE 33.9% (highest in sector) | Order Book ₹1,643 Cr (+75% YoY since FY23) | EBITDA Margin 16.4%

⚠️ Risk: GETCO = 29% revenue. BTW-Atlanta lost ₹14 Cr in FY25. 86x P/E post +117% from IPO.

GE Power India (GVPIL) — Hidden Value-Unlock in Power Sector

GVPIL CMP ₹579 | MCap ₹3,936 Cr | Power EPC & Services

• Moat: GE Vernova’s India arm. Sole authorised service provider for every GE turbine/generator in India — captive, recurring, high-margin • 3 Value-Unlocks: BHEL Settlement ₹340 Cr | JSW Demerger (10 JSW per 139 GVPIL, BSE/NSE approved) | ICRA upgraded BBB+ Stable • Q3 FY26: Revenue ₹386 Cr (+22%) | PAT ₹72 Cr vs ₹(18.6) Cr loss | EBITDA +339% | Near-zero debt • Valuation: 19x P/E vs BHEL 174x / Siemens 82x — cheapest in power EPC

⚠️ Risk: Order intake -59% in 9M FY26. Normalized EBITDA margin 14–15%. CFO resigned April 2026.

🚀 GE Power’s demerger & value unlocks are ideal for systematic algo strategies. Ask Our StyrkeX Algo Experts How to Build Strategies Around Event-Driven Stocks Like GVPIL → StyrkeX — NSE empanelled & SEBI registered.

Indo Tech Transformers (INDOTECH) — South India’s 50-Year Champion

INDOTECH | CMP ₹2,414 | MCap ₹2,506 Cr Power / Transformers

• Q3 FY26: PAT ₹24.90 Cr (+29.2% YoY) — 7th consecutive quarterly improvement | Near-zero debt • Margins & ROE: Operating Margin 16.81% (highest ever, above 16% for 3 quarters) | ROE 30% in FY25 vs 15.5% 5-year average • Valuation: 39x P/E — cheapest high-ROE transformer. TARIL 70x, Atlanta 86x | 56,000+ transformers deployed • Tech moat: DuPont Amorphous Core (98%+ efficiency) | 400 kV EHV facility

⚠️ Risk: Small cap ₹2,506 Cr — limited liquidity. Southern SEB payment delays. Already +119% from 52W low.

Side-by-Side: All 5 Stocks Compared

💰 Ready to start investing in these stocks? Create Your Free Algo-Ready Demat Account with Dhan — Start Investing Today → Advanced order types, API trading — built for data-driven investors.

📞 Not sure which stock fits your risk profile? Book a Free 1-on-1 Portfolio Strategy Call — Get a Personalised Investment Plan →(https://ohfjkpo5qed.typeform.com/launchoffer) Our experts build structured, research-backed portfolios. Limited slots.

📱 Want live stock updates & real-time alerts? Follow @pmtrades on Instagram — Daily Stock Analysis, Signals & High-Conviction Ideas → Thousands of investors follow live market moves and sector deep-dives every day.

Disclaimer: Educational only. Not investment advice. Consult a SEBI-registered financial advisor. Past performance is not indicative of future results.

Frequently asked questions

Which is the best Indian stock to buy in 2026?

GE Power India (19x P/E) for best risk-reward. Indo Tech for value (30% ROE at 39x). MTAR for long-term growth (Bloom 7x + Nuclear).

What is India’s transformer supercycle?

Surge in transformer demand from grid expansion. India added 86,433 MVA in FY25. Driving Atlanta (+117%) and Indo Tech (+119%).

Is GE Power India undervalued?

19x P/E vs BHEL 174x and Siemens 82x with three simultaneous value-unlocks. Risk: order intake -59% in 9M FY26.

Is Lloyds Metals a good long-term stock?

Net debt-free, ₹12,286 Cr revenue, Tata Steel MoU, 55 MTPA expansion. Risk: single mine, ₹33,000 Cr capex.

StrykeX — Editorial